The Project is able to exhibit superior projected economics due to its close proximity to major infrastructure including, railway, electrical power and a deep-sea port coupled with exceptional access to highly skilled cost effective labour.

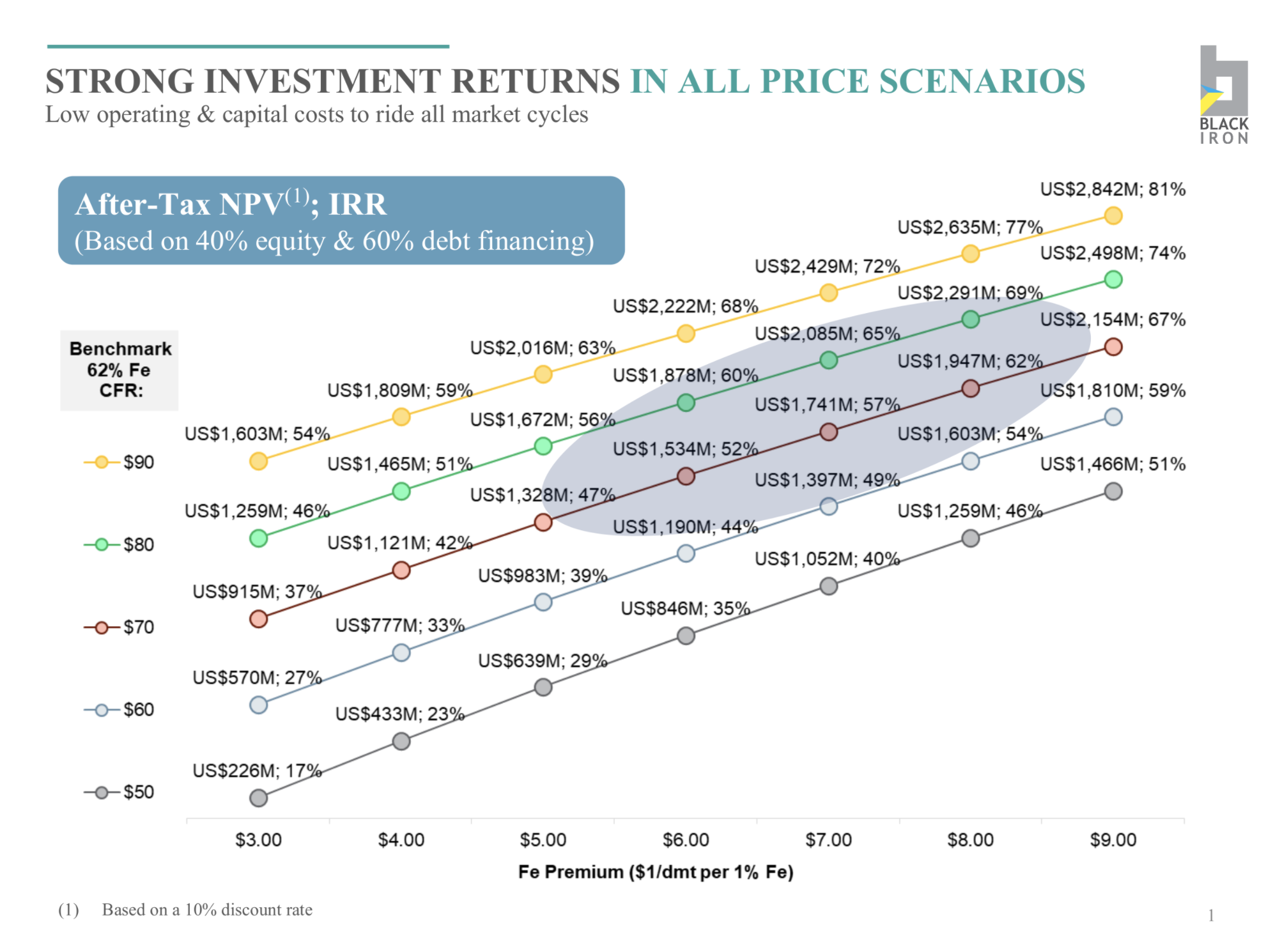

The PEA assumes a long term selling price of US$61.88/dmt for product containing 62% iron content delivered (i.e. CFR) North China adjusting using a premium of US$7.21/dmt per 1% Fe above 62% Fe, which equates to $43.28/dmt for Black Iron’s 68% Fe product, and applying a trace element premium (for silica, phosphorus and alumina), net of penalties, of $3.57/dmt of concentrate. Shipping costs to north China of US$11.54/dmt are then subtracted resulting in the FOB selling price of $97.19/dmt. The economic return at various 62% iron benchmark prices and grade premiums are shown in the table below. As can be seen, the projected economics are spectacular at higher iron ore prices while still being quite compelling in depressed pricing scenarios.

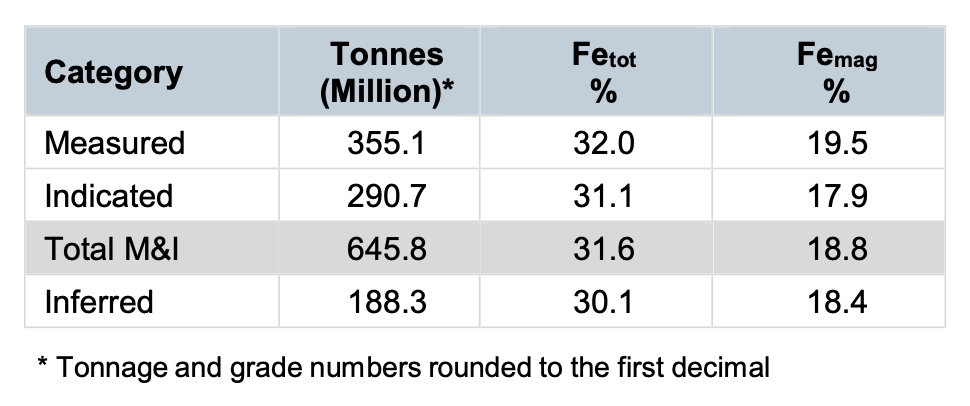

- The resource is defined by approximately 37,000 meters of historical drilling.

- Potential for resource expansion from further drilling at depth.

- National Instrument 43-101 compliant resource report and engineering studies completed.